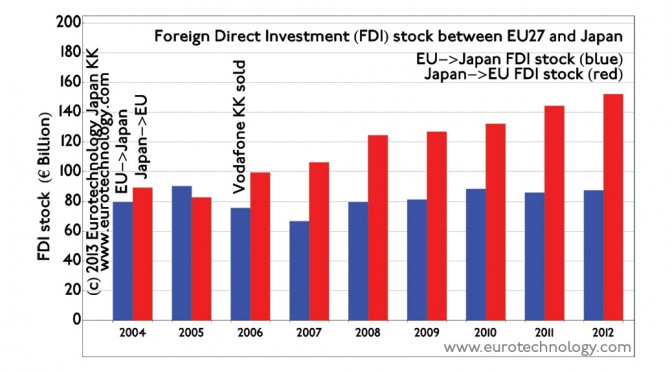

EU investments in Japan have been relatively constant around EURO 80 billion. There has been a marked reduction in EU investment in Japan in 2006 due to the withdrawal of Vodafone from Japan with the sale of Vodafone KK to Softbank for approx. EURO 12 billion (find details of the Vodafone-SoftBank M&A transaction here). This reduction of EU investment stock in Japan is clearly visible in the graphics below in 2006 and 2007.

Japanese investments in EU are steadily increasing, as Japanese companies are seeking to grow business outside Japan’s saturated market, and as Japanese companies acquire European companies for market access, technology and global business footprint. In 2012 the total investment stock of Japanese companies in the EU-27 has reached around EURO 150 billion.

Taking advantage of low EURO exchange rates and the high YEN, and low valuations during the current economic crisis, Kyocera acquired 93.84% (51,968,300 shares) of TA Triumph-Adler AG at a purchasing price of € 1.90/share for a total purchase price on the order of € 98.7 Million.

Kyocera acquired TA Triumph-Adler for its distribution network: TA Triumph-Adler has about 35,000 companies as customers in 33 countries, with 70% of sales in Germany, giving Kyocera a much larger distribution footprint in Germany and EU.

Kyocera launched the new brand “TASKalfa” for a new type of micro-particle toner for copy machines and a new software platform for copiers

Triumph-Adler

Triumph was founded 1896 as a bicycle maker, and has grown into a major European office equipment manufacturer and sales company. Triumph used to be famous for typewriters, with the disappearance of typewriters, Triumph went through a long sequence of restructuring and through many merger and acquisition transactions by many different owners including: Litton Industries, Volkswagen AG, Olivetti, Ideal Loisirs.

TA Triumph-Adler’s annual sales are € 298.5 million.

Read our report on Japan’s electronics industry sector to learn more about Kyocera and its place in Japan’s electronics industry sector:

Stuart Chambers, CEO of NSG Group, gave a press conference on October 16, 2008, here are some notes and thoughts.

On February 16th, 2006, Nippon Sheet Glass’ offer for the 80% of Pilkington plc it did not already own, for US$ 3.14 billion in total, was accepted by Pilkington’s share holders and the acquisition was completed in June 2006. At the 142nd Annual Shareholder Meeting on June 27th 2008, Stuart Chambers was appointed Representative Executive Director, President and CEO of NSG Group.

Here some essential points of Stuart Chambers’ presentation, entitled “Four critical factors for Japanese corporates making major international acquisitions”.

The four critical factors in the title are:

Integration (share holders and customers demanded integration, because the value of the combined NSG + Pilkington after the acquisition must become bigger than the sum of its parts -> must change HR management, and board)

Repaying debt -> senior management must understand the balance sheet

Identifying growth opportunities for the future (glass for solar energy)

Succession

From the outset the aim was not to create a Japanese company with overseas subsidiaries, but to create an international company, headquartered in Japan and listed on the Tokyo Stock Exchange. Therefore the greatest changes needed to be made in Japan.

NSG Group changed from an exclusively Japanese Board, to a new Board structure:

Board of Directors: 12 (7 Japanese + 5 non-Japanese) and

Executive Officers: 23 (11 Japanese + 12 non-Japanese)

These changes were necessary in order to retain non-Japanese management talent from leaving the acquired company after the merger.

The Board structure was changed from the traditional Kansayaku (Corporate Auditor) structure to a Board with Committees.

HR management changes from internal promotion according to time served in each job level to the international practice of combining internal and external hiring according to capability and demonstrated performance ignoring age as a factor.

The Israeli company Iscar has completed the acquisition of Japanese competitor Tungaloy Corporation. Iscar acquired more than 90% of outstanding shares for around US$ 1 billion from Nomura Principal Finance Co.

Iscar is the world’s second largest maker of tungsten carbide cutting tools, and competitor Tungaloy is the world’s fifth largest. Iscar is controlled by Warren Buffet’s Berkshire Hathaway Inc. – Berkshire Hathaway acquired 80% of Iscar for US$ 4 billion in 2006.

The merged Iscar and Tungaloy will be better positioned to compete with global leader Sandvik AB, which has sales on the order of US$ 4 Billion.

Tungaloy Corporation emerged via a management buyout from Toshiba Tungaloy, with Nomura Principal Finance Co. as the largest share holder. Tungaloy has sales of YEN 50 Billion (approx. US$ 500 million), was founded in 1934, and has 2618 employees. Tungaloy is the fifth largest maker of Tungsten Carbide cutting tools in the world.

Iscar entered Japan’s market by opening a 100% owned subsidiary company in 1994, about 14 years ago.

To my knowledge this acquisition is also far larger than any acquisition in Japan by any European Union (EU) company this year (last year, in 2007 Permira announced the acquisition of Arysta LifeScience Corporation for US$ 2.2 Billion and completed the deal during 2008). The three largest acquisitions ever of Japanese companies by EU companies have been Vodafone’s acquisition of J-Phone (transaction value: about US$ 20 Billion), Daimler’s acquisition of Mitsubishi Motors (transaction value: about US$ 2-3 Billion), and Renault’s investment in Nissan (initial transaction value: about US$ 3 Billion) – of these three, only the Renault investment in Nissan was successful, the other two failed.

Copyright notice:

Warren Buffet: Warren Buffett at the 2015 SelectUSA Investment Summit.

With the very high EURO and low valuations of many Japanese companies, and with changing attitudes in Japan, now is an excellent time for European companies to start or expand business in Japan.

There are many ways to start or expand business in Japan, and acquiring a Japanese company is one of the paths often selected by European companies to grow in Japan.

Some acquisitions of Japanese companies by European corporations have led to fantastic successes – while others have led to catastrophic failures.

The presentation will discuss the key factors for European companies to succeed in acquiring a Japanese company, and some of the key reasons for failure, based on the speakers 23 years of experience with Japan’s high-tech sector.

Two practitioners from Tokyo will debate the changes in Japanese attitudes to mergers and acquisitions. During the course of this seminar, we will cover M&As between Japanese companies, the slow impact of foreign investment into Japan, and the outward investment strategies of Japanese companies.

Speakers:

Dr Gerhard Fasol, President, Eurotechnology Japan KK

David Syrad, Managing Director/Managing Director Asia, A.K.I. Japan Limited

Time and Date:

Friday April 18, 2008, Sandwiches: 12:30, Seminar: 13:00-14:30