Despite being the world’s third largest market, many businesses struggle to break into Japan. The “Growing your Business in Japan” free webinar, organized by the SCI’s Science and Enterprise Group and powered by LabLinks, will provide valuable insights into the challenges of growing a chemistry-facing business in the Japanese market, and how they can be overcome. The host, Dr Alan Steven – Chief Scientist at CatSci Ltd and Co-founder of LabLinks, will be joined by:

Featuring speakers with pharma, intellectual property and entrepreneurship backgrounds, this webinar is a great opportunity to learn about the potential strategic pitfalls when entering the Japanese market and how Japanese culture can affect how a business performs in Japan. The free webinar will be held on Tuesday 31st January 2023 at 09:00 – 11:00 GMT

Do not miss the opportunity to meet the speakers, network, participate in open discussions, and gain first hand knowledge on how to successfully enter the Japanese market.

Sanofi acquires SSP (エスエス製薬株式会社), a Japanese OTC pharmaceutical company, founded as a pharmacy in Tokyo in 1765

Boehringer Ingelheim had acquired SSP (エスエス製薬株式会社), a Japanese OTC pharma company founded originally in 1765 as a pharmacy in Yaesu, Tokyo, starting with business cooperation, followed by staged investment over a period of five years, starting in 1995, followed by a Take-Over-Bid and delisting of SSP from the Tokyo Stock Exchange in 2010.

History, and acquisition steps by Boehringer Ingelheim:

SSP (エスエス製薬株式会社) was founded in 1765 as a pharmacy in Yaesu, Tokyo

On 29 October 1927 the company was incorporated as (株)瓢箪屋薬房

In 1940 the company name was changed to (エスエス製薬株式会社)

1969 IPO on the 2nd section of the Tokyo Stock Exchange

1971 IPO on the 1st section of the Tokyo Stock Exchange

1995-1996 Boehringer Ingelheim invests in SSP, and becomes largest share holder

2001 Boehringer Ingelheim increases shareholding to above 50%

15 February 2010 Boehringer Ingelheim Japan Investment GK (ベーリンガーインゲルハイム・ジャパン・インベストメント合同会社) issues a Take-Over-Bid (TOB), which is concluded on 15 April 2010, resulting in Boehringer Ingelheim Investment Japan acquiring a total of 93% of SSP shares.

16 July 2010 SSP is delisted from Tokyo Stock Exchange

1 October 2010 merger with Boehringer Ingelheim Japan Investment GK (ベーリンガーインゲルハイム・ジャパン・インベストメント合同会社)

19 November 2010 merger with BI Nippon Invest GK (BIニッポンインベスト合同会社)

19 November 2010 becomes subsidiary of Boehringer Ingelheim Japan KK (ベーリンガーインゲルハイムジャパン株式会社)

“Mr. Suzuki didn’t want to be a VW employee, and that’s understandable” (Prof. Dudenhoeffer via Bloomberg)

Suzuki Volkswagen divorce: Volkswagen makes approx US$ 1.3 billion profit, Suzuki comes out more or less even

by Gerhard Fasol, All Rights Reserved. 18 September 2015, updated: 27 September 2015

Suzuki Volkswagen divorce. “Mr. Suzuki didn’t want to be a VW employee” (Prof. Dudenhoeffer via Bloomberg). What can we learn?

A smiling Martin Winterkorn and Osamu Suzuki (79 years old at that time) looking the other way celebrated their freshly agreed “comprehensive partnership” at a press conference in Tokyo on December 9, 2009. Friends of mine who attended this press conference told me later that the lack of communication between Martin Winterkorn and Osamu Suzuki was quite visible to the audience, and that they already then had doubts about the future of this partnership.

Its interesting to look at the faces of Mr Winterkorn and Mr Suzuki in Reuters’ photograph of the occasion – a beaming Mr Winterkorn, and Mr Suzuki looking away from Mr Winterkorn – avoiding Mr Winterkorn’s eyes.

Wall Street Journal reported, that Suzuki and Volkswagen would negotiate details of their “comprehensive partnership” sometime later weeks or months after the announcement. We now know that these negotiations did not lead anywhere, and were never concluded.

Reuters reports that at the press conference VW CEO Martin Winterkorn focused on his plan to overtake Toyota as the global No. 1 carmaker in 2018 or earlier, Suzuki being obviously meant as a step to achieve this target to overtake Toyota and become No. 1 globally. According to Reuters, Volkswagen sold 3.265 million cars in the first half of 2009, and Suzuki sold 1.15 million – if combined, if Suzuki would become Volkswagen’s subsidiary, this would be 4.42 million compared to Toyota’s 3.564 million.

Suzuki Motor Corp. CEO Osamu Suzuki is reported by Reuters to have emphasized that he wanted to clear up any misunderstanding: he definitely did not want Suzuki to become a 12th brand for Volkswagen, and he does not want other people to tell him what to do – in reply to the question if he could see a German CEO for Suzuki Motor Corporation.

Suzuki Volkswagen alliance

Suzuki Volkswagen alliance time line

9 Dec 2009: VW-CEO Martin Winterkorn and Suzuki-CEO Osamu Suzuki announced the “comprehensive partnership” at a press conference in Tokyo

9 Dec 2009: Suzuki transferred 107,950,000 treasury shares to Volkswagen AG, valued approx at 226,695,000,000 yen (= approx. US$ 2.3 billion)

Suzuki acquired a 2.5% voting stake in Volkswagen for US$ 1.13 billion

15 Jan 2010: VW purchased 19.89% of Suzuki shares for about € 1.7 billion

Sept 2011: Suzuki’s Board decides to terminate the partnership

18 Nov 2011: Suzuki gives notice to Volkswagen of termination of partnership, Volkswagen does not reply

24 Nov 2011: Suzuki files for arbitration at International Court of Arbitration of the International Chamber of Commerce (ICC) in London

30 Aug 2015: ICC Arbitration Court issues judgement and holds the termination of the partnership valid, orders VW to sell all Suzuki shares back to Suzuki, and orders Suzuki to pay damages for breaking the agreement

17 Sep 2015 8:45am: Suzuki purchases back 119,787,000 of its own shares previously owned by VW back via Tokyo Stock Exchange ToSTNeT-3 system for 460,281,547,500 yen (approx. US$ 3.9 billion)

26 Sep 2015: Suzuki announced the transaction to sell all 4,397,000 Volkswagen shares which Suzuki owns to Porsche Automobile Holding SE, completing the termination of the partnership and capital alliance with VW

No common language, colliding expectations and no “meeting of minds”

Much has been reported in the press about what went wrong with the Suzuki-Volkswagen alliance, and both parties obviously have a very different understanding of the development, and both sides will feel obliged to maintain confidentiality. The ICC arbitration is also confidential. Therefore it will be hard to establish the precise facts.

However, it is obvious, that from the start there was no “meeting of minds”.

Expectations were very different and on collision, and obviously were never discussed openly between VW and Suzuki at CEO level. Even if they had wanted to, without any common language any direct communication was impossible anyway between CEOs.

Suzuki apparently hoped to receive technology from Volkswagen, Suzuki is reported to have hoped for personnel support, workers from Volkswagen (?) – it is not clear to this author what Suzuki was planning to give in return. Suzuki apparently gave up on the hope to obtain Diesel engines from Volkswagen and in the end did so from Fiat, which Volkswagen claimed to be an infringement of the cooperation agreement, a view which seems to have been maintained by the ICC arbitrators.

It is obvious, that Volkswagen was aiming to acquire increasing stakes of Suzuki, and was aiming to make Suzuki a subsidiary under Volkswagen control. Volkswagen was particularly interested in Suzuki’s market position in India via Maruti Suzuki India Limited, and by Suzuki’s know-how in designing and producing cost-efficient small sized vehicles. Again its unclear what Volkswagen planned to give in return.

Reportedly, Volkswagen demanded to increase the holding of Suzuki shares to 33% to “facilitate technology transfer”.

In September 2011, Suzuki Motors’ Board of Directors decided to terminate the cooperation with VW, making Suzuki Volkswagen divorce unavoidable.

On 18 Nov 2011 Suzuki gave notice to Volkswagen of termination of the partnership, and asked for return of the Suzuki shares. Volkswagen held on to the Suzuki shares for the time being.

On 1 July 2011, Suzuki-CEO Osamu Suzuki chose to inform the world in great detail about his opinion and decisions about the relationship between Suzuki and “Wagen” (ワーゲン). This article is entitled “スズキとワーゲンの今とこれから (鈴木修氏の経営者ブログ)” (english translation: “Suzuki and Wagen now and the way forward” (Osamu Suzuki’s management blog)). Osamu Suzuki’s blog can be read here (may need Nikkei subscription).

Clearly, calling Volkswagen “Wagen” and “Wagen-san” already expresses Osamu Suzuki’s frustrations very clearly. We are not sure, but most likely Volkswagen CEO and top management probably read this blog a few days later once it was translated by VW’s Japanese staff.

With this blog article it was unmistakably clear to the world that the Suzuki-“Wagen” cooperation had been broken down without any possibility for repair, and makes the Suzuki Volkswagen divorce public.

Professor Ferdinand Dudenhoeffer, Director of the Center for Automotive Research at the University Duisburg-Essen according to Bloomberg, summarized: “Mr Suzuki didn’t want to be a Volkswagen employee, and that’s understandable”.

In the same article, Der Spiegel reports that in an unnamed VW Executive’s opinion, future acquisition of a majority of shares of Suzuki by VW has been agreed since the beginning of the negotiations: clearly exactly the opposite of Suzuki-CEO Osamu Suzuki’s public statements – pointing to a huge misunderstanding between both CEOs.

On 30 August 2015, Suzuki announced details of the arbitration in London and its result in a press notice.

According to Suzuki, Suzuki requested VW to terminate the alliance and the capital relationship, but VW apparently did not respond. Therefore, Suzuki gave notice on 18 Nov 2011 of the termination, and on 24 Nov 2011 Suzuki filed for arbitration with the International Court of Arbitration of the International Chamber of Commerce (ICC). Suzuki asked for termination of the agreement with VW, and to rule that VW should sell all Suzuki shares either directly to Suzuki, or to a third party determined by Suzuki.

One 30 August 2015, the ICC ruled:

Termination of Suzuki-VW Framework Agreement: Suzuki’s termination notice of 18 Nov 2011 is valid, and the alliance therefore ended on 18 May 2012.

Divestment of shares in Suzuki: VW must sell all shares of Suzuki either direct to Suzuki or to a third party nominated by Suzuki

Suzuki’s breaches of agreement: IIC found that Suzuki violated some parts of the Framework Agreement, and that damages to be paid by Suzuki to Volkswagen will be determined later.

Lessons to learn from the Suzuki Volkswagen divorce: communication & respect

“Comprehensive partnership” without meeting of minds does not work

Partnerships are hard when CEOs on both sides don’t have any language in common, thus can’t talk to each other

Hidden agendas destroy trust

Without trust partnerships don’t work

Processes and methods (e.g. acquisitions of minor players all over Europe) successful in Europe often don’t work in Japan

Partnerships without respect both ways don’t work

Renault and Carlos Ghosn show us how to build a Japanese-European car company alliance, Daimler (with Mitsubishi Motors) and Volkswagen (with Suzuki) show us how it does not work

Suzuki Volkswagen alliance: financial aspects

Volkswagen reportedly paid Suzuki 222.5 billion yen (= approx. US$ 2.5 billion) for 19.89% of Suzuki’s shares

Suzuki acquired a 2.5% voting stake in Volkswagen for US$ 1.13 billion

On December 9, 2009, Suzuki transferred 107,950,000 treasury shares to Volkswagen AG, valued approximately at 226,695,000,000 yen (= approx. US$ 2.3 billion)

On June 3, 2010, Suzuki announced the offer of additional shares to be issued by third-party allotment to Volkswagen AG to bring Volkswagen’s share up to 19.89% as follows:

3,660,000 newly issued shares

issue price 1755 yen per share

total proceeds = 6,423,300,000 yen (= approx. US$ 64 million)

Suzuki announced to use the funds received from Volkswagen as follows:

122,484 million yen (= approx. US$ 1.2 billion) for Research and development expenses focusing on environmentally friendly, next generation technology for automobiles

100,000 million yen (= approx. US$ 1 billion) Reduction of interest-bearing liabilities to improve financial position (corresponding roughly to the purchase costs of Suzuki’s 2.5% stake in Volkswagen)

Suzuki Volkswagen divorce: financial aspects

On September 17, 2015, Suzuki announced the acquisition of treasury shares in order to acquire the shares in Suzuki held by Volkswagen AG:

Suzuki acquired 119,787,000 Suzuki common stock shares

Total amount paid: 460,281,547,500 yen (US$ 3.9 billion)

Suzuki has more than 1 Trillion yen (US$ 8.3 billion) in cash, and paid for the share purchase in cash from cash reserves.

Volkswagen had informed Suzuki to have sold 111,610,000 shares corresponding to 19.89% of voting shares, corresponding to approx. 463 billion yen ($3.8 billion).

On September 26, 2015, Suzuki announced the sale of all 4,397,000 Volkswagen voting shares Suzuki owned to Porsche Automobile Holding SE

Suzuki sold 4,397,000 Volkswagen voting shares to Porsche Automotive Holding SE

Suzuki did not announce the sales value. At VW’s current (27 Sept 2015) share price of € 115.82, the total sale revenue is expected to be approximately € 509 million (= approx. US$ 570 million)

Completion of sale: Sept 30, 2015

Suzuki reports an extraordinary profit of YEN 36.7 billion (= approx US$ 304 million) on this sale.

Ignoring transaction costs, interest, opportunity cost, arbitration and legal fees etc. the balance looks as follows:

Volkswagen purchased the 19.89% stake in Suzuki for approx. US$ 2.5 billion and sold the same stake for approx. $3.8 billion, i.e. making approx. US$ 1.3 billion profit

Suzuki sold its 19.89% shares to Volkswagen for approx. US$ 2.5 billion, and now repurchased the same shares for approx. $3.8 billion. In parallel, Suzuki purchased 2.5% of Volkswagen voting shares for approx. US$ 1.13 billion. Thus Suzuki overall, theoretically, made a small loss of approx. US$ 30 million on these transactions plus may have to pay damages to VW for breach of contract to be determined later by ICC.

Purely financially, Volkswagen made approx. US$ 1.3 billion profit on this transaction, while Suzuki came out more or less unchanged except for the damages Suzuki may have to pay to Volkswagen.

Suzuki Motor Corporation (スズキ株式会社) – slogan: “Small Cars for a Big Future”

In FY2014, Suzuki sold 750,000 cars in Japan and 1,170,000 cars in India

Suzuki Motor Corporation (スズキ株式会社) was founded by Michio Suzuki (鈴木道雄) (18 Feb 1887 – 27 Oct 1982) in October 1909 as Suzuki Type Machine Manufacturing Workshops (鈴木式織機製作所) in Hamamatsu, Shizuoka-ken.

On 15 March 1920 Suzuki-type Machine KK (鈴木式織機株式会社) was founded, and renamed to Suzuki Motor Engineering KK (鈴木自動車工業株式会社) in June 1954. In October 1990, the company was renamed to today’s name: Suzuki Motor Co Ltd (スズキ株式会社).

Suzuki’s international business includes:

Maruti Suzuki India Limited (マルチ・スズキ・インディア)

Magyar Suzuki Corporation (マジャールスズキ)

Changan Suzuki (長安スズキ)

P.T. Suzuki Indomobil Motor (スズキ・インドモービル・モーター)

In FY2014, Suzuki sold:

750,000 cars in Japan

1,170,000 cars in India

however, in 2012 decided to end car sales in the USA

Maruti Suzuki India Limited (マルチ・スズキ・インディア) – slogan: “Way of Life!”

Sanjay Gandhi first tried to cooperate with Volkswagen, cooperation attempts with Volkswagen failed, leading to cooperation with Suzuki

On 16 Nov 1970, the company ‘Maruti technical services private limited’ (MTSPL) was founded by the Indian Government to lay the foundation for an Indian automotive industry, and Sanjay Gandhi was the first CEO.

Sanjay Gandhi contacted Volkswagen AG to seek a cooperation or joint-venture to produce an Indian version of the VW Käfer (Beatle). However, a cooperation with Volkswagen did not work out. The company failed in 1977, and was reborn as Maruti Udyog Ltd by Dr V. Krishnamurthy.

In 1982, Maruti Udyog Ltd and Suzuki entered into a licensing and joint venture agreement, which has developed very well into India’s largest automotive company: today’s Maruti Suzuki India Limited (マルチ・スズキ・インディア).

publicly traded (BSE: 532500, NSE: MARUTI)

Market capitalization: 1.33 trillion Indian Rupees (US$ 20.23 billion) (as of Sept 18, 2015)

Market share in India: approx. 37% (2012) – 45% (2014) of India’s passenger car market (45% for 2014 according to Nikkei Business Online)

6900 employees

Suzuki ownership: increased from 26% to 40% in 1987, increased to 50% in 1992. Currently Suzuki owns 54% of Maruti Suzuki.

TOSHIBA sells KONE holding – fall-out from Toshiba’s accounting issues

Toshiba

TOSHIBA sells KONE holding: In the wake of Toshiba’s accounting issues, Toshiba announced the sale of its 24,186,720 shares, corresponding to a 4.6% holding in Finnish elevator company KONE for EURO 864.7 million (YEN 118 billion, US$ 0.95 billion).

TELC has sales of approx. YEN 120 billion (US$ 1.2 billion) per year, and employs about 4700 people.

KONE

KONE was founded in 1910. KONE’s annual sales are on the order of EURO 7 billion, and KONE employs about 47,000 people. KONE’s shares are listed on NASDAQ OMX Helsinki Exchange.

Idemitsu Kosan (出光興産株式会社) aims for market leadership

On December 20, 2014, both Idemitsu Kosan and Showa Shell separately announced that they had entered into discussions of possible business reorganization, indicating that Idemitsu Kosan may acquire Showa Shell next year. Because Showa Shell Sekiyu KK is a Japanese company traded on the Tokyo Stock Exchange, such an acquisition would be via a tender offer for outstanding shares.

With the development of fuel efficient cars and the shrinking population, refined oil products are a shrinking market in Japan, and a merger between Idemitsu Kosan and Showa Shell is a consequence of consolidation of this shrinking market.

This merger would also mean a departure of Royal Dutch Shell from the Japanese market.

Showa Shell Sekiyu KK (昭和シェル石油株式会社)

Listed on Tokyo Stock Exchange (TKS5002)

Market cap: YEN 384 billion (= US$ 3.2 billion)

Although Showa Shell Sekiyu KK (昭和シェル石油株式会社) generally uses the famous yellow and red Shell logo, Showa Shell Sekiyu KK (昭和シェル石油株式会社) is not a wholly owned subsidiary of Royal Dutch Shell plc, but its a public company traded on the Tokyo Stock Exchange (TSE5002), with a large number of shareholders beyond Royal Dutch Shell plc, which is the largest shareholder with a holding of 35.0%.

Given Royal Dutch Shell plc’s holding of 35.0%, this holding currently is worth approx. YEN 134.4 billion (US$ 1.12 billion).

35% of the reported tender offer price would correspond to YEN 175 billion (US$ 1.44 billion)

Revenues and market shares in Japan’s oil/gasoline markets

With a merger of Idemitsu and Showa-Shell, the combined company will have a firm second position with a 30% market share, very close to the market leader JX Holdings with 34% market share.

History of Shell and Showa Shell Sekiyu KK (昭和シェル石油株式会社) in Japan

Showa Shell Sekiyu KK (昭和シェル石油株式会社) is the basis of the Royal Dutch Shell Group in Japan.

Showa Shell Sekiyu KK (昭和シェル石油株式会社) was formed on January 1, 1985 by the merger of Showa Oil Co Ltd and Shell Sekiyu KK. The Royal Dutch Shell Group had a shareholding in Showa Oil Co Ltd since June 1951.

Shell Sekiyu KK goes back to Samuel Samuel & Co, started by Samuel Samuel in partnership with his brother Marcus Samuel, 1st Viscount Bearstead (subsequently The Lord Bearstead and The Rt. Hon. The Viscount Bearsted Bt. – the founder of the Shell Transport and Trading Company), in Yokohama around 1876. Samuel Samuel & Co set up the Rising Sun Petroleum Co Ltd. In 1947, Rising Sun Petroleum Company was renamed Shell Sekiyu.

Shell Sekiyu and Showa Sekiyu merged in 1985 to form Showa Shell Sekiyu.

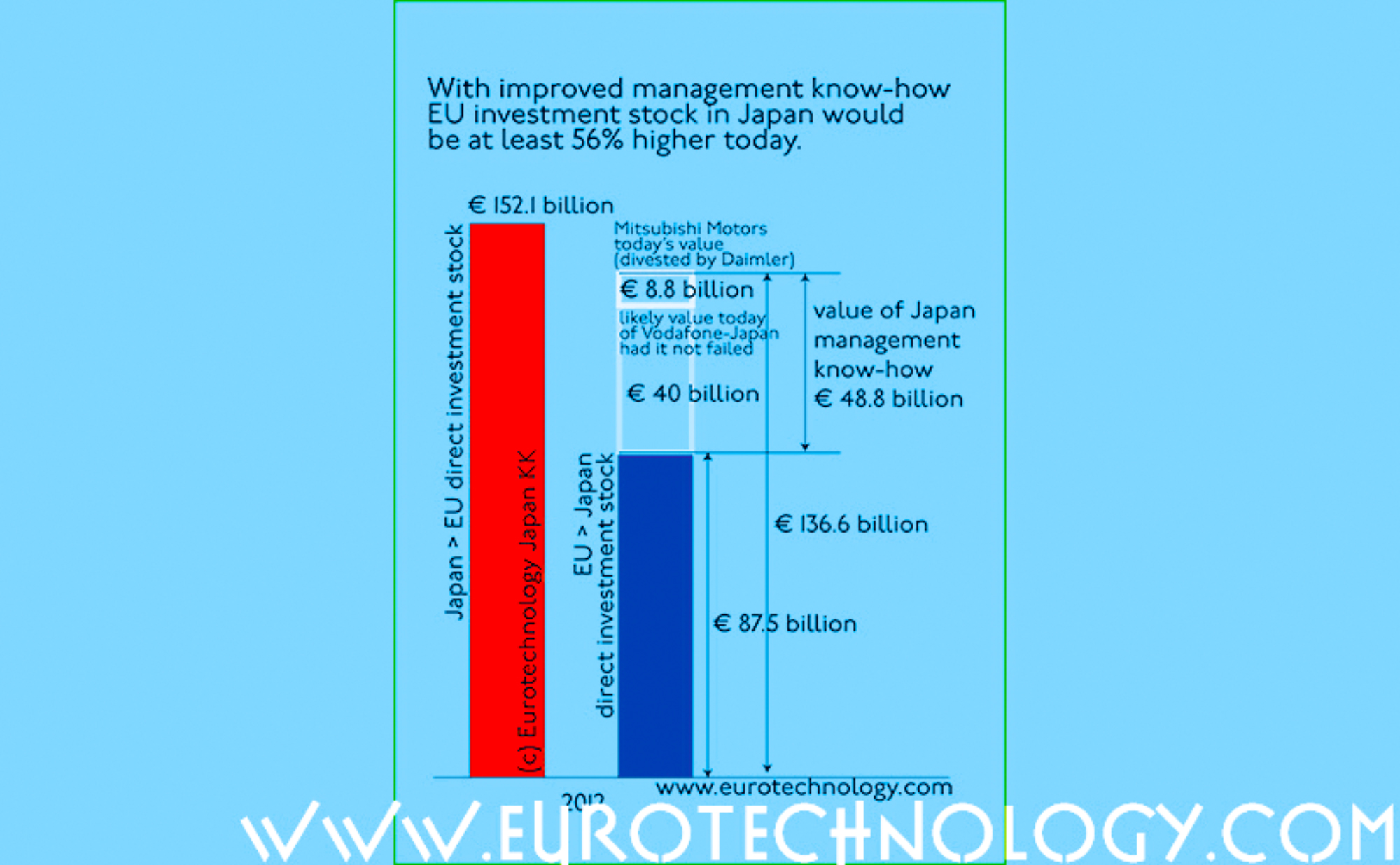

Had Vodafone succeeded in Japan, Vodafone-Japan could be worth about US$ 50 billion today, about 1/2 of Vodafone’s total global market-cap today, and combined investment in Japan by European (EU) companies could be about 50% higher than it is today!

With COLT about to acquire KVH, it might seem that this is the only foreign infrastructure based telecom provider left in Japan’s telecom market after a long string of management failures, including Vodafone, Cable & Wireless, Willcom, WorldCom and others.

However, foreign investment in Japan’s telco/cloud infrastructure has not ended, and we believe the next wave including AWS, Microsoft, Google et al may become far more successful than the first wave.

For companies considering investment or business expansion in Japan, it is useful to understand the potential market-capitalization which can be achieved in Japan in case of success, instead of just looking at the sales figures:

as an example, combined EU investment in Japan is estimated to be approx. € 85 billion (US$ 106 billion) in total,

had Vodafone succeeded in Japan, total investment in Japan by European (EU) companies would be about 50% higher than it is today.

Why Vodafone-Japan could be worth US$ 50 billion (1/2 of Vodafone’s global market cap) had it been successful

Let us estimate what Vodafone-Japan could be worth today, had it not failed:

Since Vodafone-Japan’s sale to SoftBank on March 17, 2006, Japan’s telecom market has continuously grown, so we can expect today’s valuations to be considerably higher than in 2006. Lets assume that Vodafone-Japan had been successful, and had grown in sync with competitors NTT-Docomo and KDDI, and lets assume that Vodafone-Japan would have been able to continue J-Phone’s innovations to keep subscription figures and financial results in sync with KDDI. In this case, it would not be unreasonable to assume that Vodafone-Japan’s market capitalization today would be KDDI’s minus the value of KDDI’s global data-center business. Thus we arrive at an estimate, that Vodafone-Japan would have a market-cap value on the order of US$ 50 billion today.

Thus, had Vodafone been successful in Japan, EU investments in Japan could be about 50% higher than they are today, and Vodafone’s global market cap could be 50% higher as well.

Market capitalization (Dec 2, 2014):

NTT Group: US$ 61 billion

NTT-Docomo: US$ 68 billion

KDDI: US$ 58 billion

SoftBank: US$ 80 billion

Vodafone plc (global group): US$ 97 billion

Vodafone-Japan market cap, had it been successful (our estimate): US$ 50 billion corresponding to approx. 50% of Vodafone’s global market cap)

total investment in Japan by all European (EU) companies combined: € 85 billion (= US$ 106 billion)

(see: EU-Japan direct investment register)

EU investment in Japan is about € 85 billion – it could be 50% higher!

Both Colt and KVH were founded with investments by Fidelity Investments and associated companies, Colt in London in 1992, and KVH in 1999 in Tokyo, as telecommunications service providers for the financial industry and other industrial customers. While KVH remained 100% owned by Fidelity and associated companies, Colt was listed on the London Stock Exchange in 1996.

Initially founded as telecommunications companies, both Colt and KVH have developed into “information delivery platforms” based on networking infrastructure, data centers, optical fibre networks and associated management and information services.

On November 12, 2014, Colt announced the plan to acquire KVH for YEN 18.595 billion (€ 130.3 million = US$ 160 million) in cash from KVH’s owner Fidelity Investments.

Since KVH is 100% owned by Fidelity Investments, and Colt have also been founded by Fidelity which is still a shareholder, the acquisition needs to be approved by independent Directors and by independent shareholders of Colt.

A General Meeting of Colt’s shareholder has been announced for December 16, 2014 at 10:00am in Luxembourg where the approval of shareholders of Colt will be sought.

Colt – the “information delivery platform”

Colt was founded by James P Hynes (Jim Hynes) with investments from Fidelity Investments and related companies in 1992 in London, and went public with an IPO on London Stock Exchange in 1996.

Colt operates 20 data centers and substantial optical fiber networks, and has more than 5000 employees.

Colt’s annual revenues are € 1,575.8 million (= US$ 2 billion) in 2013.

Colt market capitalization currently is UKL 1.19 billion (= US$ 1.9 billion).

KVH – “Asia’s information delivery platform”

KVH was founded by Fidelity Investments and related companies on April 2, 1999 in Tokyo.

KVH operates 9 Data Centers, owns optical fiber networks in Japan and to major financial centers in the world, and has about 590 employees.

KVH annual revenues are approx. € 133.6 million (= US$ 170 million) in FY2013, i.e. Colt is about 10 times bigger in terms of market cap and sales than KVH.

KVH owns optical fibre, ethernet, data center data infrastructure in Tokyo, Osaka and other parts of Asia. This photograph shows KVH owned cable infrastructure in the center of Tokyo

The planned acquisition values KVH at YEN 18.595 billion (€ 130.3 million = US$ 160 million), i.e. COLT is about 12 times bigger than KVH in terms of market capitalization/value.

Implications of acquisition of KVH by Colt – view as a Japan (and Asia) market entry by Colt

From the point of view of Colt, the acquisition of KVH – which has always been a sister company via the common investor Fidelity Investments, and common founder Jim Hynes – is a relatively low risk market entry into Japan and several other major Asian markets, and promises to have a very high chance of success for all parties.

We need to keep in mind, that essentially all other large scale market entries into Japan by infrastructure based telecommunication operators have failed: Vodafone, Cable & Wireless, WorldCom’s market entries into Japan’s telecom markets have all failed, and to our knowledge KVH is the only remaining internationally owned telecom infrastructure company in Japan today.

Essentially, both Vodafone and Cable & Wireless failed in Japan’s telecom markets, because they did not have the multitude of skills and know-how needed to manage a telecommunications business in Japan in a competitive manner. Colt with the acquisition of KVH acquires this know-how, and KVH at the same time has been an internationally managed company from the outset, so that Colt avoids the risks of acquiring a 100% Japanese companies such as Vodafone had done by acquiring Japan Telecom, with all the cultural issues that this entails.

At the same time, we also need to keep the scale in mind. While KVH has a market capitalization (i.e. the purchase price) of US$ 160 million, it can be argued that Vodafone-Japan could be expected to have a capitalization of around US$ 60 billion today had it been successful – i.e. about 375 times larger than KVH.

Japan’s largest telecommunication operator NTT currently has a market capitalization of US$ 62 billion, i.e. about 390 times larger than KVH, while SoftBank’s market capitalization is about 500 times larger than KVH’s.

Thus, if we see Colt’s acquisition of KVH as a market entry into Japan by a European telecom operator, then this is on an approx. 300-400 times smaller scale than Vodafone’s failed market entry into Japan, and with far better circumstances, and a far higher chance of success, and in our view with very carefully controlled risks.

Without doubt, a merger of KVH with Colt was on the minds of Fidelity Investments and Jim Hynes, when they founded both KVH and Colt in the 1990s.

Nokia to expand market share in Japan, Panasonic to focus on core business

Panasonic, after years of weak financial performance, is focusing on core business. Nikkei reports that Panasonic is planning to sell the base station division, Panasonic System Networks, to Nokia.

Nokia expands No. 1 position in Japan

Our analysis of Japan’s mobile phone base station market shows, that Nokia became No. 1 in Japan’s base station market with the acquisition of Motorola’s base station division. Acquisition of Panasonic System Networks will expand Nokia’s NSN to expand market leadership in Japan’s mobile phone base station market.

Panasonic System Networks

Panasonic System Network’s market share is estimated at around 10% of Japan’s mobile phone base station market, while international sales are essentially non-existent. Thus Panasonic System Network’s global market share is negligible, giving Panasonic little possibility for the scale necessary to operate a stable profitable longterm base station business.

Japan’s mobile phone handset makers and base station makers have for many years focused on serving Japan’s internal market only, and in particular have focused on Japan’s No. 1 mobile phone operators NTT Docomo. This gave Japan’s mobile phone base station makers a temporary home advantage, however with the value shift from hardware to software, they lack scale, and are subsequently uncompetitive globally. More about Japan’s Galapagos effect here.

The context: EU investments in Japan

While Japanese investments in Europe are booming, recently European investments in Japan have been stagnating after Vodafone’s withdrawal from Japan, and there are very few new European investments in Japan. Could it be that Nokia’s investment in Japan starts a new trend of renewed European investments in Japan?

Tokyo AIM: LSE sells its share in the Tokyo AIM joint venture to Tokyo Stock Exchange and leaves Japan

Initially, London Stock Exchange and Tokyo Stock Exchange created Tokyo AIM as a joint-venture company in order to create a jointly owned and jointly managed Tokyo AIM, modeled according to the very successful London AIM model.

Nikkei: “Tokyo Stock Exchange has learnt enough from the London Stock Exchange to set up a similar market on its own”

However, on March 26, 2012 NIKKEI reported that “Tokyo Stock Exchange has learnt enough from the London Stock Exchange to set up a similar market on its own. TSE plans to improve the rules of its own new market, so that TSE can create a more welcoming market” (our translation of the original Japanese NIKKEI article to English).

London Stock Exchange withdrew from the venture, and Tokyo Stock Exchange took over 100% of Tokyo AIM. Essentially, London Stock Exchange AIM’s venture into Japan failed, while the stock market created by the venture continues without London Stock Exchange’s involvement. As explained in our blog here, these events are very very similar to what happened with NASDAQ about 10 years earlier!

Tokyo AIM is renamed TOKYO PRO Market and TOKYO PRO BOND Market

In 2012, the name was changed from Tokyo AIM, to TOKYO PRO Market and TOKYO PRO BOND Market. Details can be found here:

Boehringer Ingelheim acquisition values SSP at approx US$ 900 million

Boehringer Ingelheim acquires SSP stage-by-stage: 9.2% in 1996, 60% in 2001, 100% in 2010

Boehringer Ingelheim acquires SSP (エスエス製薬株式会社), a Japanese OTC pharma company founded originally in 1765 as a pharmacy in Yaesu, Tokyo, starting with business cooperation, followed by staged investment over a period of five years, starting in 1995, followed by a Take-Over-Bid and delisting of SSP from the Tokyo Stock Exchange in 2010.

SSP (エスエス製薬株式会社), founded in 1765

History, and acquisition steps by Boehringer Ingelheim:

SSP (エスエス製薬株式会社) was founded in 1765 as a pharmacy in Yaesu, Tokyo

On 29 October 1927 the company was incorporated as (株)瓢箪屋薬房

In 1940 the company name was changed to (エスエス製薬株式会社)

1969 IPO on the 2nd section of the Tokyo Stock Exchange

1971 IPO on the 1st section of the Tokyo Stock Exchange

1995-1996 Boehringer Ingelheim invests in SSP, and becomes largest share holder

2001 Boehringer Ingelheim increases shareholding to above 50%

15 February 2010 Boehringer Ingelheim Japan Investment GK (ベーリンガーインゲルハイム・ジャパン・インベストメント合同会社) issues a Take-Over-Bid (TOB), which is concluded on 15 April 2010, resulting in Boehringer Ingelheim Investment Japan acquiring a total of 93% of SSP shares.

16 July 2010 SSP is delisted from Tokyo Stock Exchange

1 October 2010 merger with Boehringer Ingelheim Japan Investment GK (ベーリンガーインゲルハイム・ジャパン・インベストメント合同会社)

19 November 2010 merger with BI Nippon Invest GK (BIニッポンインベスト合同会社)

19 November 2010 becomes subsidiary of Boehringer Ingelheim Japan KK (ベーリンガーインゲルハイムジャパン株式会社)

Nippon Boehringer Ingelheim Co., Ltd. (ベーリンガーインゲルハイム ジャパン株式会社) was founded in 1961 as a subsidiary of the German Boehringer Ingelheim Group, which was founded in 1885 in Ingelheim am Rhein in 1885.

TELC has sales of approx. YEN 120 billion (US$ 1.2 billion) per year, and employs about 4700 people.

KONE

KONE was founded in 1910. KONE’s annual sales are on the order of EURO 7 billion, and KONE employs about 47,000 people. KONE’s shares are listed on NASDAQ OMX Helsinki Exchange.